Genetics helps estimate the risk of disease – but how much does it really tell us?

Genetics research has made momentous strides in the 21st century. At the start of the century, we had a broad understanding that most medical problems in the developed world are partly genetically determined but lacked the technology to fully explore the secrets hiding in our genome.

This century’s technological advances have allowed us to make substantial progress in identifying the genomic underpinnings of heart disease, mental health disorders, cancer, dementia, and other diverse diseases that medicine still struggles to prevent, diagnose and treat.

We can now quantify the overall genetic contribution (heritability) and identify specific genetic variants that contribute to the risk of these diseases. But, as with most things genetic, it’s complex, it’s incomplete and scientists are still working out how to make it clinically useful.

Each of these diseases and disorders has a “polygenic” underpinning. This means that instead of only one or a few genes playing a role in the risk of diseases, it is likely to be thousands of genes where inherited changes in each gene make a modest impact on our risk of each disease. This dispersed genetic component combines with other environmental risk factors – such as smoking, diet, trauma and stress - to further increase or decrease our risk of ill health.

This polygenic underpinning is good news in many ways: our risk is determined by multiple genetic variants and usually not by a single yes/no genetic risk factor. Some single genetic risk factors do exist, such as variants in the BRCA1 and BRCA2 genes that substantially increase the risk of breast and ovarian cancer. But these single-hit genetic variants are rare – meaning that, for most of us, genetic predisposition comes from the combined risk of many variants.

Genetic studies over the past 20 years have identified many such variants that contribute to the polygenic loading for disease: more than 100 for breast cancer, depression and coronary artery disease, and 38 for Alzheimer’s disease. All these variants can give us information on the underlying biology and new targets for drug development. These variants can also contribute to the calculation of risk scores, indicating those who are at genetically high risk of disease and those who are at low risk.

The term “score” is appropriate here because it can be calculated by simply adding up the number of high-risk genetic variants carried across the genome, weighted by the importance of each variant.

If you look at polygenic scores for a large group of people, most people will have a score that is near average, so their genetics adds little information to their disease risk. A few people will have a high polygenic score, putting them at increased risk of developing a particular disease. Others will have inherited few risk variants, putting them at lower risk of disease.

So are polygenic scores useful? Potentially, yes, but mostly no – not yet. Polygenic scores can give us a personal estimate of our genetic risk for a certain disease, which remains constant throughout life and can be calculated at any point. They could give an impetus to lead a healthy lifestyle, undertake appropriate screening, or be watchful for early symptoms.

Polygenic scores are not available through the NHS but can be derived from the genetic data generated by direct-to-consumer genetic testing companies, such as 23andMe, and ancestry companies, such as AncestryDNA. These companies test your DNA from a mailed-in saliva sample and give you the option to download your genetic data to your desktop.

23andMe shows you information on your polygenic risk of type 2 diabetes. And websites such as impute.me allow you to upload your own genetic data to calculate your polygenic scores.

Making sense of your score

The MyGeneRank app gives you your coronary artery disease score on your phone by linking to your 23andMe genetic data. This sounds wonderfully accessible, but what can your coronary artery disease polygenic score actually tell you? First, it can tell where your risk lies compared with other people of the same genetic ancestry as you. For example, if MyGeneRank tells a person that their polygenic score lies at the 55th percentile of the distribution, then their risk lies very close to average.

What about someone who is at the 95th percentile, in the top 5 per cent of people with the highest genetic risk? That might be worrying information, but to interpret a polygenic score you need two further pieces of information. First, you need a “relative risk”: how much does your polygenic score change your risk compared with an average person? Does it double your risk or increase it tenfold? Second, you need a “lifetime risk”: what is your chance of being diagnosed with the disorder?

These figures depend on your genetics, how many people develop the disease and how much of the disease risk the polygenic score explains, which is small for most diseases. For example, a woman with a breast cancer polygenic score in the top 1 per cent of the population has a lifetime risk of about 30 per cent. For most disorders, lifetime risks are lower.

A high polygenic score for schizophrenia might be worrying news for people, but our genetic knowledge of schizophrenia is far from complete. The estimated chance of developing schizophrenia for someone with a high polygenic score, seen only in one in 100 people, is 4 per cent compared with a 1 per cent risk for most of the population. This result may be reassuring, but also shows that schizophrenia polygenic scores should not be used clinically. We have developed an online tool to calculate how the lifetime risk of disease changes at different levels of polygenic scores.

Polygenic scores give you a snapshot of your genetic risks, but for most disorders, the partial information captured is not strong enough for it to be useful. The next decade will determine whether polygenic scores remain a personal curiosity, or whether they become an important medical tool.![]()

Cathryn Lewis, Professor of Genetic Epidemiology & Statistics, King's College London and Oliver Pain, Postdoctoral Research Associate, King's College London

This article is republished from The Conversation under a Creative Commons license. Read the original article.

An asteroid impact could wipe out an entire city – a space security expert explains NASA’s plans to prevent a potential catastrophe

The Earth exists in a dangerous environment. Cosmic bodies, like asteroids and comets, are constantly zooming through space and often crash into our planet. Most of these are too small to pose a threat, but some can be cause for concern.

As a scholar who studies space and international security, it is my job to ask what the likelihood of an object crashing into the planet really is – and whether governments are spending enough money to prevent such an event.

To find the answers to these questions, one has to know what near-Earth objects are out there. To date, NASA has tracked only an estimated 40 per cent of the bigger ones. Surprise asteroids have visited Earth in the past and will undoubtedly do so in the future. When they do appear, how prepared will humanity be?

The threat from asteroids and comets

Millions of objects of various sizes orbit the Sun. Near-Earth objects include asteroids and comets whose orbits will bring them within 120 million miles (193 million kilometers) of the Sun.

Astronomers consider a near-Earth object a threat if it will come within 4.6 million miles (7.4 million km) of the planet and is at least 460 feet (140 meters) in diameter. If a celestial body of this size crashed into Earth, it could destroy an entire city and cause extreme regional devastation. Larger objects - 0.6 miles (1 km) or more - could have global effects and even cause mass extinctions.

The most famous and destructive impact took place 65 million years ago when a 6-mile (10-km) diameter asteroid crashed into what is now the Yucatán Peninsula. It wiped out most plant and animal species on Earth, including the dinosaurs.

But smaller objects can also cause significant damage. In 1908, an approximately 164-foot (50-meter) celestial body exploded over the Tunguska river in Siberia. It leveled more than 80 million trees over 830 square miles (2,100 square km). In 2013, an asteroid only 65 feet (20 meters) across burst in the atmosphere 20 miles (32 km) above Chelyabinsk, Russia. It released the equivalent of 30 Hiroshima bombs worth of energy, injured over 1,100 people and caused US$33 million in damage.

The next asteroid of substantial size to potentially hit Earth is asteroid 2005 ED224. When the 164-foot (50-meter) asteroid passes by on March 11, 2023, there is roughly a 1 in 500,000 chance of impact.

Watching the skies

While the chances of a larger cosmic body impacting Earth are small, the devastation would be enormous.

Congress recognized this threat, and in the 1998 Spaceguard Survey, it tasked NASA to find and track 90 per cent of near-Earth objects 0.6 miles (1 km) across or bigger within 10 years. NASA surpassed the 90 per cent goal in 2011.

In 2005, Congress passed another bill requiring NASA to expand its search and track at least 90per cent of all near-Earth objects 460 feet (140 meters) or larger by the end of 2020. That year has come and gone and, mostly due to a lack of financial resources, only 40 per cent of those objects have been mapped.

As of Feb. 14, 2022, astronomers have located 28,266 near-Earth asteroids, of which 10,033 are 460 feet (140 meters) or larger in diameter and 888 at least 0.6 miles (1 km) across. About 30 new objects are added each week.

A new mission, funded by Congress in 2018, is scheduled to launch in 2026 an infrared, space-based telescope – NEO Surveyor – dedicated to searching for potentially dangerous asteroids.

Cosmic surprises

We can only prevent a disaster if we know it is coming, and asteroids have sneaked up on Earth before.

An asteroid the size of a football field – dubbed the “City-killer” – passed less than 45,000 miles from Earth in 2019. An asteroid the size of a 747 jet came close in 2021 as did a 0.6-mile (1-km) wide asteroid in 2012. Each of these was discovered only about a day before they passed Earth.

Research suggests that one reason may be that Earth’s rotation creates a blind spot whereby some asteroids remain undetected or appear stationary. This may be a problem, as some surprise asteroids do not miss us. In 2008, astronomers spotted a small asteroid only 19 hours before it crashed into rural Sudan. And the recent discovery of an asteroid 1.2 miles (2 km) in diameter suggests that there are still big objects lurking.

What can be done?

To protect the planet from cosmic dangers, early detection is key. At the 2021 Planetary Defense Conference, scientists recommended a minimum of five to 10 years’ preparation time to mount a successful defense against hazardous asteroids.

If astronomers find a dangerous object, there are four ways to mitigate a disaster. The first involves regional first-aid and evacuation measures. A second approach would involve sending a spacecraft to fly near a small- or medium-sized asteroid; the gravity of the craft would slowly change the object’s orbit. To change a bigger asteroid’s path, we can either crash something into it at high speeds or detonate a nuclear warhead nearby.

These may seem like far-fetched ideas, but in November 2021, NASA launched the world’s first full-scale planetary defense mission as a proof of concept: the Double Asteroid Redirection Test, or DART. The large asteroid Didymos and its small moon currently pose no threat to Earth. In September 2022, NASA plans to change the asteroid’s orbit by crashing a 1,340-pound (610 kg) probe into Didymos’ moon at a speed of approximately 14,000 mph (22,500 kph).

Learning more about what threatening asteroids are made of is also important, as their composition may affect how successful we are at deflecting them. The asteroid Bennu is 1,620 feet (490 meters) in diameter. Its orbit will bring it dangerously close to Earth on Sept. 24, 2182, and there is a 1 in 2,700 chance of a collision. An asteroid of this size could wipe out an entire continent, so to learn more about Bennu, NASA launched the OSIRIS-Rex probe in 2016. The spacecraft arrived at Bennu, took pictures, collected samples and is due to return to Earth in 2023.

Spending on planetary defense

In 2021, NASA’s planetary defense budget was $158 million. This is just 0.7 per cent of NASA’s total budget and just 0.02 per cent of the roughly $700 billion 2021 U.S. defense budget.

This budget supports a number of missions, including the NEO Surveyor at $83 million, DART at $324 million and Osiris Rex at around $1 billion over several years.

Is this the right amount to invest in monitoring the skies, given the fact that some 60 per cent of all potentially dangerous asteroids remain undetected? This is an important question to ask when one considers the potential consequences.

Investing in planetary defense is akin to buying homeowners insurance. The likelihood of experiencing an event that destroys your house is very small, yet people buy insurance nonetheless.

If even a single object larger than 460 feet (140 meters) hits the planet, the devastation and loss of life would be extreme. A bigger impact could quite literally wipe out most species on Earth. Even if no such body is expected to hit Earth in the next 100 years, the chance is not zero. In this low likelihood versus high consequences scenario, investing in protecting the planet from dangerous cosmic objects may give humanity some peace of mind and could prevent a catastrophe.![]()

Svetla Ben-Itzhak, Assistant Professor of Space and International Relations, West Space Seminar, Air War College, Air University

This article is republished from The Conversation under a Creative Commons license. Read the original article.

The top automation trends in the insurance industry for 2022

In the search for a personalised experience, consumers are forcing insurers to adapt to their demands

Thanks to technology, we’re all used to speed and personalisation in our personal and professional lives. When a fast food app can greet you by name and ask if you want your favourite meal again, you expect that kind of customer experience from every company.

The insurance industry should offer the best possible customer service and the most personalised experience. After all, it deals with the most important parts of our lives, from health to safety to our family’s futures. And it’s all possible through AI-based automation, from machine learning (making predictions based on data and learned experiences) to deep learning (using non-linear algorithms to model abstract relationships in historical data). So what are the trends in automation coming up for 2022 and how is insurance going to look different at the end of the year?

Incorporating individual preferences

The most obvious trend driving the insurance industry that benefits from automation is consumer personalisation. From shopping to entertainment, our expectations for personalised experiences have changed. Customers want speed, customisation and recognition of personal preferences, and insurers can actively meet their demand for individualism.

Insurers can’t afford to lag behind. According to Policy Advice, nearly 90 per cent of consumers want more personalised insurance products and policies. And, according to a JD Power survey, more than one-third of consumers say they’re interested in usage-based car insurance (using technology to track driving habits and adjusts accordingly). The volume of customer interactions already using that technology has doubled.

Channel switching is another common expectation from customers looking for individualized service and flexibility. Insurers predict the volume of inbound communication will increase substantially, and nearly two-thirds of consumers want to communicate using a variety of digital options – not by making a phone call. That means the insurance company has to have a platform to offer a unified experience.

Experts estimate there’ll be up to 1 trillion connected devices by 2025. This means devices in our everyday lives continually learn more about us, our preferences and our surroundings. Of all the industries leveraging that data with data science to build powerful AI, insurance is one ripe to benefit most by connecting data to products, claims and customer service.

Optimising operational efficiencies

The insurance industry is moving into a digital-first economy with successful firms quickly optimising their operations and making them more efficient. While AI can’t (and shouldn’t) replace human connection and intuition, there’s no denying that AI’s ability to find, digest and analyse huge amounts of data far exceeds most teams of analysts. That capability translates to a number of big business benefits.

- Better pricing. Working with large pools of data allows for very specific solutions that save time and reduce the margin of error from prices that don’t line up with costs. For example, a home insurance company could use AI to quickly analyse geographical location, marital status and other factors to come up with pricing very specific to that person and that house. In effect, using data instead of intuition as a guide allows for very specific offerings and lets insurance companies develop them more quickly than a purely manual effort.

- Faster response time/higher response rate. Insurance companies are investing in AI-enabled systems to crunch and learn from claims data more quickly than human beings and boost customer satisfaction. From a bottom-line perspective, that means companies will be processing more claims, faster and more accurately. All of this increases volume throughput (without necessarily increasing staffing costs) and reduces waste in the claims processes.

- Increase employee engagement/reduce turnover. No matter what the form of automation, it reduces and in some cases eliminates rote work from employees’ daily responsibilities. If you look at a call centre as one example, customer service agents won’t have to deal with the same query over and over again, especially when it’s a simple question. Automation takes the ‘blah’ out of business and replaces it with employee engagement.

Insurance agencies will use artificial intelligence to boost their bottom lines, market share and operational efficiencies in 2022.

Integrating with ease

Organisations are going to take sophisticated artificial intelligence and easily integrate it into their automation flows in 2022, especially when organisations are able to apply AI intentionally and narrowly. With AI embedded into their capabilities, low-code/no-code platforms provide a win-win for the IT team, the organisation and the users (both customers and brokers/agents who have to adapt to new tools).

And while insurance carriers have lagged behind other industries such as retail, one of the benefits of investing in AI-based solutions later is that the insurance sector is learning from other industries, reducing the time and cost of integration and adoption. Insurers will continue to seek and onboard SaaS solutions with enterprise-grade SDKs and powerful APIs to support modernisation efforts alongside their existing technological investments.

The benefits outweigh the costs

Change is hard. Adopting new technology that also changes how you work can be even harder. Customer service representatives may have to learn new roles. Brokers and agents may need to adopt different ways of interacting with customers. None of those changes are fixed overnight.

There is both a tangible and an intangible cost to adopting AI-driven tools and technologies. But the benefits of AI are so clear to both the company and the consumer, and the pace of adopting AI is going to be so fast in 2022, that it’s critical to embrace that change for everyone’s benefit.

To find out more, visit ushur.com

by William Roberts, Senior Product Marketing Manager and Meredith Barnes-Cook, Global Head of Insurance & Industries, Ushur

INDUSTRY VIEW FROM USHUR

Rethinking risk can unshackle Africa’s small scale farmers from the grip of poor weather

Right now, countries in the Horn of Africa are in the midst of a multi-season drought. There have also been years in which the rains have come with such force that floods wash out the season’s labour, sometimes along with homes, as happened in Mozambique just two years ago.

Climate change is making these disasters more common. It is hard for rural families whose livelihoods depend on the food they can grow. A 2015 study by the World Bank estimated that climate change over the next 20 years would increase the number of desperately poor people by 122 million, if nothing was done about it.

While the drivers of deep-seated poverty in rural Africa are many and complex, climate shocks are one of the most important.

Research I’ve done with colleagues in the past has shown how climate shocks affected rural households in Ethiopia and Honduras. We found that acute shocks – a devastating hurricane or prolonged drought – could push households into chronic poverty and hardship.

Not only can climate shocks push families into poverty, it can also keep them there. The dreaded anticipation of shocks, or risk, discourages investments that could otherwise raise families’ living standards and reduce their vulnerability to poverty. From the Sahel to Central America, small-farm households keep their modest savings in the form of food stocks. While understandable, indeed optimal given the constraints they face, this behaviour closes the vicious circle of shocks, risk and poverty.

But there may be a way to reset this relationship between risk, shocks and poverty. An emerging body of evidence reveals that new risk management tools that make households resilient to shocks further empower them to invest more in available technologies and economic opportunities.

My recent work in Mozambique and Tanzania , with colleagues (more on this later), adds to this evidence, showing what farmers can achieve by combining these tools.

Tools and their limitations

One of these risk management tools is agricultural index insurance. It provides payments in the event of crop losses, so a household doesn’t lose everything in a bad year. Experiments with index insurance have shown that when protected, farmers increase investment in their farms by as much as 30%, and reap matching increases in income.

I was involved in what has been one of the most successful index insurance interventions to date. In a 2010 collaboration, researchers from the International Livestock Research Institute, the University of Wisconsin and Cornell University launched a scheme like this for pastoralist households in northern Kenya. In 2015, it was adopted by the Government of Kenya and paid out over US$10 million to vulnerable pastoralists in the first five years.

Emerging evidence also shows that genetically encoded risk management technologies can achieve some of the same benefits as financial instruments. They include stress-tolerant crop varieties.

Both types of resilience-building technologies – financial and agronomic – have shown considerable promise but also have limitations. Insurance can be an expensive way to manage risk. It also brings costs each year whether or not insurance pays out.

An improved seed variety has no such continuing costs. Beyond the initial, substantial cost of developing the new variety, the seeds can be reproduced and purchased for little more than any other seed variety. But the seeds only protect farmers against specific peril (limited flooding or a specific type of drought). Beyond this they provide little or no protection.

Surprising result

These observations suggested to us that bundling different risk management technologies might be the way to unshackle Africa’s small-scale farmers from the vicious circle of shocks, risk and poverty.

In Mozambique and Tanzania, my colleagues and I conducted a four-year randomised control trial that combined index insurance and stress-tolerant maize to exploit the synergies of both together. The insurance expanded the protection that the seeds gave. The seeds’ tolerance of some drought reduced the cost of the insurance. It would also provide higher yields than other varieties even in normal years.

We designed the bundle so that in a severe drought, seeds would be replaced and farmers would be able to plant again in the next season with the same stress-tolerant seeds.

The project had a surprising result: farmers who experienced the steepest losses to drought grew a bigger harvest than they ever had before in the year immediately after.

When we analysed the data, we found that insured farmers could not only feed their families following a drought, they also increased the amount of improved maize seed they purchased. In fact, they invested more improved seed than they ever had before. Those additional purchases drove the increase in yields in the following year as farmers became convinced that the technologies worked, enabling them to deepen their investment and increase their incomes.

A new ending to the same old story

These and many other field trials are building evidence that effective tools to manage risk can create a new ending to the same old story about shocks, risk and poverty. These tools not only protect current well-being and promote resilience, but can also provide a solid foundation for future improvements. Together, resilience to shocks and the resulting investments into growing more food build what we call Resilience+.

Accelerating climate change has made it especially urgent to create flexible bundles that improve resilience.

If tools are effective and provide value, farmers will use them to increase their agency to choose improved inputs, to expand or diversify their planting, or to try new and unfamiliar practices that may produce more food. We believe this approach could have a transformative impact where risk is primarily what holds families back from stronger livelihoods.![]()

Michael Carter, Professor of Agricultural and Resource Economics, University of California, Davis

This article is republished from The Conversation under a Creative Commons license. Read the original article.

Does Insurtech really deliver?

Insurtech full-stack carriers struggle to find a sustainable business model, but insurtech is more than start-ups and D2C

Insurtech has come of age. Over the past few years, around $60 billion has been invested in start-ups focused on insurance innovation. The variety of these should remind us that insurtech is more than online distribution. Even insurance incumbents – traditionally considered averse to change – have recognised the relevancy of technology and data for sustaining their competitive position. In the past 14 months, we have seen players such as Allstate and Travelers sharing their commitment to innovating the way risks are assessed, managed and transferred. Insurtech is definitely more than start-ups.

I previously wrote about the journey of Archimede SPAC and Net Insurance, highlighting that it has kept its promise.

We have heard concerns about the insurtech trend, mainly driven by the falling evaluations of the listed US full-stack insurtech carriers. I have been pretty critical over the years about their approaches and financials, aiming to stop insurance innovation professionals from adoring the wrong idols.

A player such as Lemonade is able to fascinate the minds of many insurance professionals by talking about giving back to charity, behavioural economics and business models based on charging a fixed fee. This has allowed it to become the insurtech poster child and represent the foundation of its highest evaluation at almost $10 billion in the first months of 2021.

Instead, the company today has a cap of around $1.2 billion, with around $1 billion in cash among its assets. Many of the aspects – welcomed with enthusiasm from commentators – seem like great tales, but they had a small business impact. Back in 2018, I investigated its iconic ‘slice of pizza’ mechanism. Now, it is interesting to observe its financials.

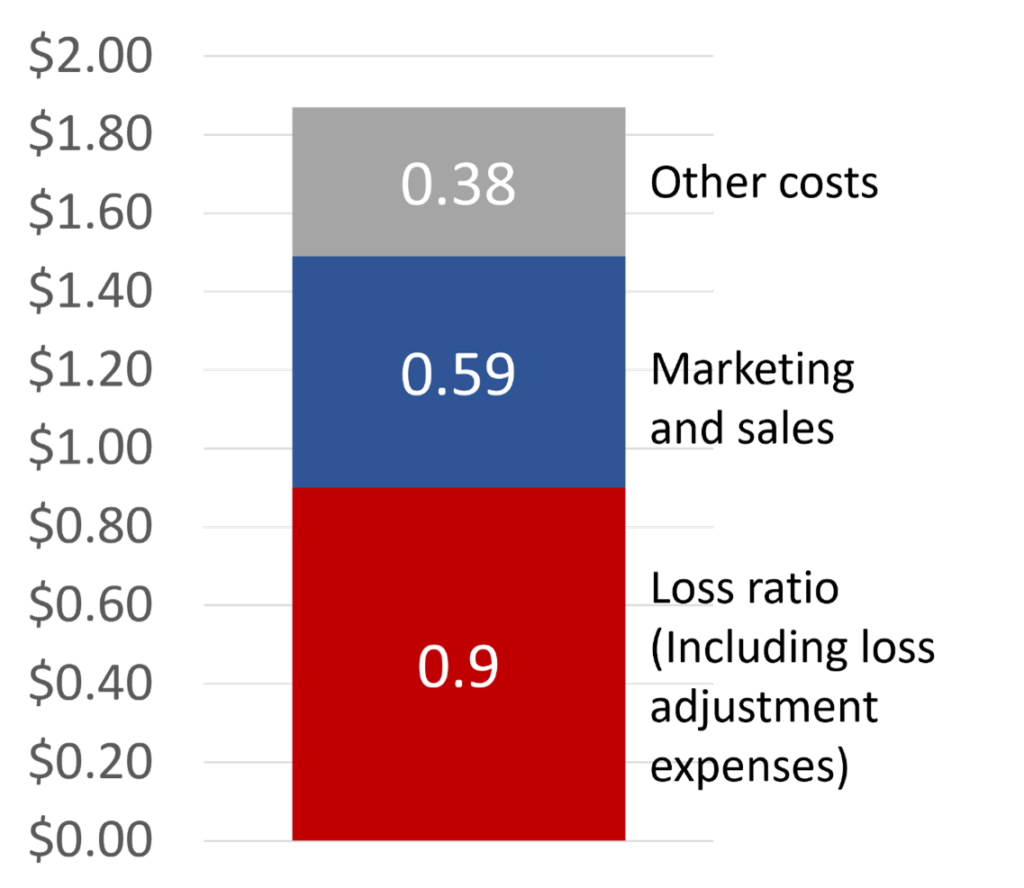

Lemonade has written almost $370 million in premiums (showing 42 per cent growth from 2020) with a combined ratio (gross of reinsurance) above 180 per cent in 2021. This means that, for each dollar of premium paid by the client, its risk transfer approach cost more than $1.80.

Back in the day, Lemonade’s mantra was about some behavioural economics mechanisms that should contain their claims: “Knowing you’re not in conflict with your insurer, and that you embellish claims at the expense of a cause you believe in, may change your behaviour, too, setting off a virtuous cycle. Ultimately, we’re after a new Nash equilibrium, one where aligned interests breed trust, resulting in a product that is inexpensive, hassle-free and lovable.”

Its policyholders’ behaviours don’t seem positively modified by the above mechanisms. For each dollar of premium, claims cost 90 cents, including the loss-adjustment expenses, which is far higher than the market average. To acquire this business, Lemonade has also spent almost 60 cents in marketing for each dollar of premium, and all other costs added almost 40 cents.

Lemonade’s incapacity to disrupt the insurance sector, or even change it a little bit, should not lead to any reasoning about insurtech capability successfully delivering its promise.

I believe insurtech approaches have a strong potential for improving the way risks are assessed, managed and transferred. There are many different start-ups and incumbents’ initiatives out there that are showing great returns on the innovation investment and can be used as inspiration.

To find out more, subscribe to the monthly newsletter Insurtech Facts & Figures

By Matteo Carbone, Founder and Director, IoT Insurance Observatory