Insuring autonomy

How collaborative mobile robots accentuate the need for new liability models

The stellar growth of e-commerce in the past two years has also accelerated technological progress in warehouses and fulfilment centres. Footages of gliding discs performing angular dance routines with towering shelves mounted on them have been impressive enough. But as the checked patterns of magnetic strips and wires on the floor give away, their autonomy is just an illusion.

More recently, it’s autonomous mobile robots (AMRs) that are stealing the show. They are easier to deploy and tailor to seasonal changes in demand, as they’re not guided by meshes embedded in the floor but by maps stored in their software. They are capable of planning multiple routes, picking the optimal one and pivoting to another if they see an obstacle blocking their way.

Although there seem to be lights-out warehouses and hazardous environments at the end of the road where AMRs will keep completely to themselves, today they are overwhelmingly cobots that need to work with their human peers.

Not unlike self-driving cars, AMRs have the long-term potential to make their environments safer as a result of eliminating human error. However, they are likely to present some new risks before eventually delivering on this promise. Despite their sophisticated presence detection and collision avoidance systems to safeguard against accidents, there is always a certain level of probability that they will make a mistake thanks to some momentary connectivity error.

For the same reason, cybersecurity is also a major concern. Hacking into fleet management networks controlling tens or hundreds of AMRs can cause much more serious property and bodily harm than a compromised connected doll for small children using invectives – or other amusing examples of breaches into IoT devices, where security is now a long-overdue afterthought.

Autonomy is also heavily reliant on the collection of real-time data, which makes data privacy concerns on closed factory floors – and especially in public spaces – very hard to ignore.

The need for a new liability model

At the core of the complexity of insuring autonomy there lies a feature that all autonomous vehicles from AMRs to crop-harvesting machines share: they don’t behave as humans do. In order to insure them, you need specialty underwriters who reply on subject matter experts, rendering premiums unaffordable.

Establishing liability is going to be a much more intricate process with AMRs. As accidents with self-driving cars have already demonstrated, the lines between machine and human liability can become particularly vague in this area.

But even when autonomous vehicles are the obvious ones to blame, it can get rather difficult to ascertain whether it has been the AMR hardware, the operation (security, user management, database) or functional software (navigation, path planning), the proprietary hardware or components from third parties that have led to the accident.

Machine-learning algorithms can compound the problem even further, as they enable autonomous robots to pick up new behaviours after they have been installed. The line between what the robot does because it was manufactured that way and what it’s learnt from its environment – a robotic version of the nurture/nature dilemma – will become harder to draw.

Entering the autonomy pool

Large insurers that have had policy offerings for more traditional types of robots for years are currently the most likely candidates to address these ambiguities and eliminate the grey areas that underwriters of autonomy risk need to navigate.

But what these incumbents are in acute need of is massive amounts of data to understand how these autonomous mobile systems work, what types of errors they are prone to and what the controllable and insurable risks are around their operation.

This is probably the reason why we see partnerships between big insurers and technology start-ups springing up in the autonomy space. In Korea, a country at the cutting edge of robotics, telecom firm KT Corp – in a bid to diversify into the robotics sector – has partnered with DB Insurance Co. Within the framework of this partnership, KT Corp will collect data on robotic errors and accidents for a year, which, in turn, will be fed into the insurance of service robots that DB Insurance is to develop.

In the self-driving car arena, AXA, a company owning a stake in a leading self-driving software start-up, has used UK research projects to gather data with a view to creating insurance products for autonomous vehicles.

Founded in 2020, Pittsburgh-based start-up Koop Technologies has also identified autonomy as an emerging opportunity in the insurance market. In 2021, it was selected for Lloyd’s Lab’s latest cohort, which had data and models as one of its three major themes. To supply insurers with the next level of autonomy data, it has built an API. Data collected through this API on how dropouts and disengagements affect security, as well as the ratio of miles per harmful event, will contribute to drawing more detailed and reliable risk profiles of AMRs and autonomous vehicles.

Koop, which is still in the early stages of its entrepreneurial journey, has most certainly put its finger on a problem that stands in the way of the adoption of autonomous solutions across a wide range of sectors. However, many more similar start-ups and insure-tech-incumbent partnerships need to follow in Koop’s steps to reach scale globally.

Zita Goldman

Why big firms are rarely toppled by corporate scandals – new research

Everyone makes mistakes. And that includes the world’s biggest companies, which are reliably prone to gaffes, errors of judgment and wrongdoing.

Some of these moments could even be labelled as corporate scandals – the kind of incident which shoves firms into the spotlight and places their activities under detailed public scrutiny.

But do these events do lasting damage? Does an oil spill, fraudulent activity or other unethical behaviour really affect highly valued reputations, sales and market value?

Our research suggests not. In fact, our analysis of the effects of a wide variety of business scandals shows that only rarely is the effect as severe as we might imagine.

Instead, it seems the public has a strong tendency to forget and move on. And even initial unplanned (and at the time unwanted) attention can lead to greater brand awareness, proving the old adage that any publicity is good publicity.

Take the recent furore over Spotify. In early 2022, the world’s largest music streaming service was accused by science and health professionals of offering a platform for misinformation about Covid.

So what happened next? At first, there was a dip in the stock market price of about 12 per cent when artists including Neil Young, Joni Mitchell and Graham Nash announced they were withdrawing their music from the service. This financial hiccup was followed by an immediate stock price rebound that is likely to climb beyond pre-scandal levels. Spotify went on to add disclaimers to its Covid-related content and removed some content.

So in the long term, this will probably turn out to be nothing more than a slight bump in the road for Spotify. As a business, it provides a hugely popular service and boasts 172 million premium subscribers around the world, 28 million of whom joined in 2020. How many of them will cancel their subscriptions and forgo access to their carefully curated playlists because Young and Mitchell have decided to walk?

And while it is true that the company’s business model relies on musicians and other content providers, the reality is that most artists cannot afford to not be on the platform. Giving Spotify the benefit of the doubt, it’s entirely possible it made an honest mistake and underestimated how sensitive some people have become to discussions about the pandemic. Customers will probably make peace with this.

Likewise, Netflix will doubtlessly survive recent controversies over some of its content, such as the British comedian Jimmy Carr’s comments about the Holocaust. With so many subscribers around the world attracted by the service’s wide range of content, Netflix is another example of an industry giant that can shrug things off.

And remember Facebook’s market collapse after it was linked to the personal data of millions of users being collected by the political consulting firm Cambridge Analytica? Don’t feel bad if you don’t, it lasted about seven seconds (OK, maybe seven days). The company then recovered all of the US$134 billion (£102 billion) it had previously lost in market value.

Law and disorder

So what makes some scandals stick? In our research, we found that only certain scandals tend to have significant negative effects on corporate reputations and performance. One apparently vital element is a company being found liable in a court of law. The legal process gives weight and depth to a scandal that might otherwise have quickly disappeared.

The Volkswagen emissions scandal for example, started in 2015. Seven years later, the company is still negotiating settlements in class action lawsuits brought against it for cheating on emissions tests.

The company’s share price dropped 30 per cent immediately after the scandal (it has improved since the move towards electric vehicles) and Volkswagen’s reputation is still tarnished by the event, as it continues to attract significant regulatory scrutiny, affecting its status among investors.

Similarly, years after being found responsible for the Deepwater Horizon disaster in the Gulf of Mexico in 2010, BP is still paying the price of its negligence, as it continues to be embroiled in many lawsuits. And following regulatory intervention, German financial services provider Wirecard is not even around anymore to tell the story of how €1.9 billion (£1.6 billion) disappeared from its balance sheet.

Yet without corporate culpability determined by the court of law, very few accusations stick, even in the face of media scrutiny. Without clear evidence of harm caused to a group of people, there is very little in the way of measurable negative impact, or demand for compensation for the damage caused.

As consumers, we often like to signal moral superiority and enjoy some of the drama provided by the corporate discomfort of a juicy scandal. But our research found that people’s response to a company is driven by more mundane considerations. These are price, convenience, loyalty, ease of use and habit – and there aren’t many scandals considered quite scandalous enough to make us change any of those.![]()

Irina Surdu, Associate Professor of International Business Strategy, Warwick Business School, University of Warwick

This article is republished from The Conversation under a Creative Commons license. Read the original article.

Insurance of the future: A world of evolution or revolution?

The insurance industry dates back more than 300 years – and insurers need to change their business models to survive

We live in a world where our data is shared digitally across many platforms and ecosystems. Consumers are inherently digital and consider omnichannel interactions and faster transaction processing to be the norm, not the exception.

Yet in the insurance sector, an industry steeped in tradition, companies are yet to fully embrace digitisation and keep pace with customers’ changing lifestyles and needs.

Business processes and customer touchpoints, embedded in organisations for decades, are being swept away by online and app-based companies powered by the Cloud, APIs (tools enabling products, services and systems to easily integrate with a network of partners), data analytics, mobile devices and social media.

Looking ahead, insurers with technology platforms that allow them to instantly respond to market demands, trends and disruptors, develop new business partnerships, source new revenue streams and offer additional products and services – while guaranteeing online responsiveness, performance and reliability – will thrive.

Those who fail to adopt new business models, innovate quickly and find additional ways to engage with existing and new customer bases will inevitably cause their own demise.

Composable enterprises

Insurers of the future must morph into composable enterprises. This maximises their ability to build, assemble and reassemble core business elements, seize market opportunities and respond to disruptors and threats while maintaining resilience.

Gartner, in its 2022 Insurance Industry Trends survey, found only 8 per cent of insurance CIOs have a composable enterprise strategy in place – so what’s the starting point for leadership teams?

- Focus on making changes to growth strategies, architecture and technology

- Adopt a modular mindset

- Add new components to existing legacy systems (to support new ecosystem connections and exposure to new markets/revenue streams)

Insurers need to answer questions around future business plans, ecosystems and whether their architecture has the structural capability to adapt and repurpose propositions, with composable software components in place (these interconnected pieces drive the technology necessary to support business growth).

Rather than remove legacy systems, which have great business value, businesses should support them with modular technology platforms such as microservices architecture. It connects separate or ‘decoupled’ elements and supports interlinked software applications, enabling communication via the Cloud. They can then be managed, modified, tested, deployed and scaled, without affecting the wider operation.

Kleber Bacili

CEO at Sensedia

INDUSTRY VIEW FROM SENSEDIA

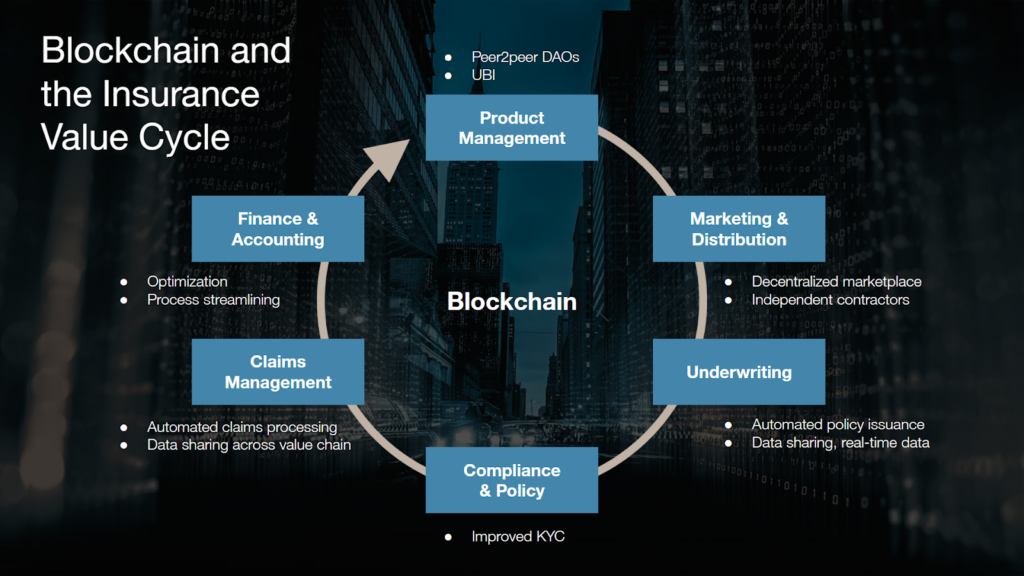

Blockchain: threat or opportunity for the future of insurance?

Could blockchain technology bring a simpler, more efficient way to provide, buy and consume insurance?

Looking at the global market for blockchain-based insurance, the figures don’t seem particularly impressive. In fact, research by Markets and Markets expects it to reach just £1.39 billion by 2025. A paltry sum compared with the anticipated value of the global insurance industry, which Swiss Re Institute expects to top $7 trillion in 2022.

But the compound annual growth rate (CAGR) and the figures tell a different story. The growth in traditional insurance is estimated in the low-to-middle single digits, whereas blockchain-based insurance has a CAGR of almost 85 per cent. In fact, Gartner estimates blockchain will top $3.1 trillion in new business value by 2030, which represents a huge opportunity for insurance companies and their InsureTech vendors.

It’s time for change

As the industry has grown and flourished, so has it fragmented and atomised, with insurers at one end, claims processors at the other – and reinsurers, managing general agents and brokers in between – all consuming a slice of the pie.

It is in this environment that inefficient exchange of information has also flourished, as multiple parties with different priorities communicate with each other using different systems and processes – to the point where the industry wastes a lot of time, money and resources just maintaining a “complex ecosystem”.

Blockchain can help overcome many of these challenges.

Simplifying complexity

Blockchain’s decentralised quality means it can simplify, expand and accelerate information exchange, while ensuring anyone on any machine, software or system can access the blockchain. This is made even more powerful by ensuring only authenticated, approved users can write data to the blockchain. Moreover, blockchains are protected by consensus protocols, which reduce the likelihood of fraud and malfeasance.

Automating the claims process

Blockchain also can help do away with manual claims processing and reviewing with smart contracts. For example, insurer and insured create a digital agreement (a smart contract) that says every time the latter drives their car, they’re insured up to, say, $5 million, with a $500 excess. And through the use of “oracles”, which connect blockchains to external systems, predetermined conditions can be fed into the blockchain, activating a smart contract based on real data from the outside world.

In fact, Lemonade has built its entire business case on the fact that the vast majority of claims can be processed nearly instantaneously.

Blockchain can empower every stage of the insurance life cycle

Dynamic insurance or usage-based insurance

Dynamic insurance made a big impact during the Covid-19 outbreak, with many car insurance users speaking out against paying a yearly premium when they were unable to drive. Since then, however, usage-based insurance has skyrocketed, affecting various fields. But most interesting is the use of external real-world data to calculate premiums.

Today the technology exists to tell if a driver is drunk behind the wheel, speeding, running red lights or driving without due care and attention. Link all this data together and you can create dynamic products that charge people premiums based on their risk in real-time, rather than on “average”. This would certainly make car insurance fairer and cheaper, and limit low-risk drivers footing the bill for “boy racers”.

The insurance industry is already moving towards a pay-per-use model. With the rise of car clubs and fractional ownership, paying for car insurance by the hour or the day is now commonplace. The trick for insurers will be to package this into a smart contract that’s automated, transparent and ID-verified.

A picture of health

Similarly, health insurers could take a comparable approach using real-time health data from wearable apps such as Fitbit and Apple Watch to adjust premiums by the hour, day or week. Again, technology exists to achieve this but using the blockchain to record and feed all this personal data would allow insurers to link it easily and directly to a specific individual.

Added protection

You can also eliminate policyholders’ concerns around data security by using zero-knowledge proof (ZKP), so individuals have complete control over who accesses, shares, or uses their personal data. Ultimately, it’s about creating tailored, equitable and best-value insurance to meet an individual’s specific lifestyle needs and real-life risk profile, not one based on the average.

Peer-to-peer insurance

On the downside, blockchain, for all intents and purposes, could also democratise insurance. It allows groups to pool their premiums, self-organise and self-administer their own insurance against a certain risk. Similar to peer-to-peer lending, and other DAOs, peer-to-peer insurance would allow a group of people to effectively set up their own insurance firm. Each pool member has a say over when insurance is or isn’t paid out, and smart contracts could go a long way in making the criteria for pay out simple, removing the need for any intermediaries.

There’s also the benefit of full transparency, including on fees, from the claim (when the smart contract is triggered) to payment. This makes the whole process smoother and faster as all the data, documentation and verification has been done already during the process.

Instant finality, compliance ready

In insurance, it is important transactions take place and are recognised in real-time. Recording data two days later won’t cut it. Any blockchain solution has to offer instant finality, so that transactions are recognised, finalised and executed simultaneously.

Insurance is also highly regulated, and insurers can’t insure without knowing who a counter-party is, where their money’s coming from and where it’s being sent. In fact, KYC non-compliance can result in huge fines. So having an integrated ID layer at the protocol level is a must when it comes to the highest levels of security, transparency, legal enforceability and the inevitable regulatory compliance.

Last word

Imagine a world in the not-too-distant future where an individual’s digital identity is controlled via the blockchain. For the insured, it means having complete control over their information and who gets to see, use or share it (whether the actual or ZKP information). For the insurer, it means the ability to tailor insurance based on countless off-chain data sets in real-time to make premiums more attractive to certain risk profiles. But perhaps more importantly, it’s about simplifying and automating insurance, streamlining processes and ensuring people pay premiums that reflect their real-life exposure to specific risks. All part and parcel of today’s empowered consumer.

Concordium’s decentralised layer-1 blockchain technology offers unrivalled security, privacy, transparency and control. It is the only layer-1 on the market with an ID framework which ensures accountability, responsibility and certainty in an uncertain world. Alongside our Reg DeFi Lab we understand that the DeFi space will continue to evolve and gain traction with enterprise and institutional clients. That is why we are partnering with start-ups and tech giants alike, looking to take advantage of blockchain technology. Visit Concordium to find out more.

INDUSTRY VIEW FROM CONCORDIUM

How blockchain can transform insurance

In 2020, more than 30 per cent of small businesses were uninsured, even though 75 per cent of business owners reported experiencing an insurable event that year. One pivotal reason is that navigating the traditional insurance market can be challenging for small businesses, which can face long and complicated claims processes – if they’re even able to secure insurance in the first place.

Blockchain-based parametric insurance can help address some of these needs as it issues payouts automatically according to predetermined events (rather than through a manual and inefficient claims process). Developments in blockchain technology are making parametric insurance solutions from specialised providers cheaper, faster, and more accessible for social good.

Parametric insurance smart contracts are digital agreements on blockchains with conditions attached to their execution (if x occurs, execute action y). Oracle networks, such as the clear industry-leader Chainlink, provide the necessary real-world information from outside the blockchain to confirm that conditions for payment have been met and that the insurance company should therefore pay out the claim. Blockchains keep an immutable record of transactions, providing accountability. Smart contracts improve efficiency by automating contracts. And oracle networks, which connect blockchains to real-world data, validate that an event did indeed occur and that the automated payment cannot be manipulated.

Here are four blockchain-based parametric insurance products that small businesses can use to maximise their operational security and minimise risk.

Crop insurance

According to parametric crop insurance provider Arbol, $1 trillion of agricultural risk is not insured. Much of this risk is located in developing nations, where many farmers do not have access to insurance at all. Smaller farmers, or those facing highly variable weather conditions, may also struggle to receive the coverage they need. Climate change will exacerbate the need for crop insurance as weather patterns become less predictable and extreme weather events become more frequent.

Parametric crop insurance that helps farmers secure economic protection is already live, with providers such as Arbol making it available to anybody with a smartphone. Arbol uses Chainlink to create insurance contracts around weather data from the National Oceanic and Atmospheric Administration (NOAA). For instance, a farmer could receive a payout if data from the oracle network indicated their region received less than 20 inches of rain over a two-month period.

Access to insurance prevents farmers from needing to uproot their families and abandon their farmland in years where they face unfavourable weather conditions. They can also benefit from quickly disbursed aid, while insurance providers are assured that the process is accountable, transparent and fraud-proof because all activity happens on-chain and payouts are determined by verified external conditions.

Flight and travel delay insurance

Anybody who flies knows the slow dread that accompanies the realisation that a flight has been delayed or cancelled. Though airlines will compensate fliers for cancellations, delays may cause them to miss important events or connecting flights with little recourse other than booking new, expensive last-minute replacements. Insurtechs are emerging to meet flight insurance needs, and providers leveraging blockchain technology, such as Ensuro and Etherisc, will help the space advance further. Parametric insurance allows a traveler to quickly repurpose the funds and purchase a new ticket, as compensation is automatically distributed as soon as a flight is cancelled or delayed.

Logistics and supply chain insurance

Businesses are often uninsured for improbable events that nonetheless have the potential to be catastrophic. For example, prior to the Covid-19 pandemic, very few businesses had purchased (or even had the choice to purchase) pandemic insurance, leading to a last-minute surge in demand. Parametric insurance for logistics can cover highly variable and rare events, from pandemics to extreme weather. Additionally, using oracle networks to connect IoT sensor data to blockchains, supply chain companies can purchase parametric insurance to mitigate any potential quality control issues such as losses from shipment quality issues, particularly for perishable goods.

One of the benefits of parametric insurance is the ability to tailor contracts. For instance, a supply chain company with operations vulnerable to winter storms may take out a policy to protect against disruptions. It may not be clear when, or to what extent, an ice storm could lead to delays. A parametric insurance policy can source NOAA data about ice accumulation in the relevant region and pay the policyholder accordingly. Whether the storm delays shipments by hours or days, the supplier is protected.

Connecting IoT device data to blockchains via oracles can also improve shipment quality data. Refrigerated unit sensors could inform a parametric insurance policy that pays out if temperature fluctuations compromise product safety. Oracles connected to sensors such as PingNET would trigger the payouts. With these contracts, payouts are much faster than the quality tests typically required for claims processes for spoiled goods. There’s also the added benefit of knowing that when a shipment arrives, it is in good condition, as safety issues would be recorded on-chain prior to delivery.

Live event insurance

Live events such as concerts and sports are sensitive to inclement weather (as well as, it turns out, rare, catastrophic events such as pandemics). Parametric insurance can help, as these niche events are not likely to secure insurance through traditional brokers. Event organisers can use parametric insurance to absorb cancellation losses, helping them mitigate risk and smooth out the impact of cancelled events.

Parametric insurance would protect organisers in the case of event cancellations that require refunding all attendees or rescheduling, which creates additional logistical challenges. However, parametric insurance can also help if event attendance is simply suppressed (for instance, if icy conditions prompt 20 per cent of attendees to skip the event because they don’t want to drive). Variability can be built into the parametric insurance contract, allowing event organisers to secure the exact amount of coverage they need. Mark Cuban, an investor in the blockchain-based climate data project dClimate, pointed out in a recent Wall Street Journal interview that the Dallas Mavericks could benefit from this type of weather insurance.

To learn more please visit chain.link/use-cases/social-impact

INDUSTRY VIEW FROM CHAINLINK LABS

Making the home ownership dream a reality

Estelle and her husband James rented their home in the Sacramento Valley area of California for years. They never thought they would become homeowners, but when their landlord passed away and the chance to buy their house came up, it seemed like too good an opportunity to turn down.

As is often the case, the process wasn’t entirely straightforward. The landlord’s family wished to avoid involving estate agents, and when Covid-19 hit, lenders grew reluctant to loan money to first-time homebuyers. A historic tax transcript issue also led to unforeseen complications.

Then Estelle and James came across Lower. It was the only lender that was prepared to help them become first-time homebuyers and it helped the couple every step of the way, including navigating the requirements for a loan.

Months later, the couple owns their first home and have embarked on renovations to add their own personal touch to the place they have rented for a quarter of a century. “We are still in disbelief; even when we were signing the stack of papers we were questioning if we are really the owners now,” Estelle said. “But we are! We’ve always called this place home but now it’s officially 100 per cent ours.”

Buying a home can be challenging, particularly for first-time buyers — and especially so at the moment, with rising prices and a shortage of supply. According to the National Association of Realtors, home prices have risen by 30 per cent since 2019, while the number of homes for sale is at a record low. The average home is about $80,000 more expensive than it was pre-pandemic.

Trying to help people such as Estelle and James was the reason why Dan Snyder co-founded Lower in 2014. “We wanted to make it more accessible for consumers,” he says. “Instead of an intimidating and complex journey, where they’d have to go and talk to a big bank and maybe get turned down, we wanted to open up the whole process.”

Estelle and James

The business provides a one-stop shop to enable access to anything to do with the home-buying process, ranging from savings accounts for people to build a deposit to finding an estate agent or buying insurance to protect their biggest asset. It incorporates several unique features, including the ability for people to take a lifestyle-based home readiness assessment, which can help to determine whether buying a home is the right move for people at that time.

“As a fintech lender, we do everything from the origination to the service,” says Snyder. “We think about it from the standpoint that, no matter where the customer is in their home-buying journey, we want to be able to help them along the way. We’re trying to break down walls. If you bank with us, you shouldn’t need to apply for a home loan or check if we can get a better insurance rate for you. We should just give you a better insurance rate.”

Lower has recently launched HomePass, enabling customers to offer cash and stand out in a highly competitive market. Buyers are able to win the offer, backed by a deposit, and then get their mortgage behind the scenes.

The mobile experience is a key piece of Lower’s offering. “People spend an average of five hours a day on their phones – which is more than they do for most things such as exercising, eating and sometimes even sleeping – so we felt like a mobile-first experience, whether it’s for banking with us or during the mortgage process, was important,” says Snyder. “We built it with a consumer-obsessed mindset, based on years of experience of having worked at banks and mortgage companies that weren’t changing with the times.” Around 40 per cent of Lower’s customers are first-time buyers, well above the national average percentage of total homebuyers.

The majority of customers come directly to Lower, but the business is also building relationships with estate agents, builders and financial brokers, which can be particularly useful if people are considering buying a house in an area they’re unfamiliar with. “That can help them land the home,” Snyder says. “Realtors are still very powerful conduits in the US housing market, so we’re a big supporter of our realtor network.”

Over the past eight years, Lower has grown from seven to 1,500 employees, but Snyder is keen to stress that its focus remains very much on home ownership. “We’re a mobile-first consumer finance platform,” he says. “We help people save, plan for and buy their house and then we’ve got an estate agent arm to keep it all together. We’re not trying to do commercial loans, and we don’t do stock trading. We’re going to stick on the same path of unlocking wealth through home ownership. We want to be the best at this.”

Estelle has a very simple message to anyone who thinks the dream of home ownership may be out of reach. “Don’t give up,” she says. “There may be a few hurdles here and there, but if you want to work with a firm that really cares about helping you achieve your goal of owning your own home, Lower is there to help you. We have already recommended it to others. In the future, if the need arises, we will reach out again. Lower can make it happen!”

INDUSTRY VIEW FROM LOWER

Using gaming tactics in apps raises new legal issues

When new innovations emerge, there’s always a temptation to say that we need to rewrite the rulebook for them. Gamification has been no exception.

Gamification refers to the use of elements from gaming, often by a smartphone app, to make ordinary activities like stock trading or rideshares more engaging. It can have powerful influences on our choices, sometimes in controversial ways.

For instance, users of gamified trading apps like Robinhood have suffered huge losses, often from trading too frequently and making outsized bets on meme stocks or other assets that were too risky for them.

By designing their interfaces to make stock trading look more like a game, were these apps steering their users into dangerous trading patterns?

Regulators are examining this issue. A March 2022 consultation paper by the Board of the International Organization of Securities Commissions (IOSCO) questions whether some gamification tactics should be banned.

Gamification’s role in gig work has also raised legal questions. Gig workers seem to act a lot like employees, likely in part because of the gamification tactics that apps use to influence how, where and for how long they work.

But instead of following a growing number of courts and tribunals in Canada and abroad by confirming these workers should be treated as employees, Ontario’s government is proposing that they be brought under a complicated new framework that would give them some, but not necessarily all, of the rights that come with employee status.

Gamification’s challenge to law

As outlined in a report I worked on for the University of Toronto’s Future of Law Lab, legal decision-makers struggle with gamification. It challenges the distinction they’ve traditionally drawn between persuading people with information — which preserves their freedom of choice — and taking that freedom away through coercion or deception.

It’s also possible to capture a degree of control over people’s choices by carefully structuring and timing how you give them information, so as to exploit the mental shortcuts we all take when making decisions. Well-timed push notifications, leaderboards of popular stocks and arbitrary goals assigned to gig workers can all leverage these shortcuts to guide users towards choices that make apps money, but might not serve users’ interests.

Traditional advertising does this too, of course. But unlike a billboard or a TV commercial, a smartphone app follows us around. It can also continuously test prompts and interfaces to identify the ones that do the best job of nudging us in the direction it wants.

Some say existing rules don’t do enough to deal with gamification — that we need new ones to blunt gamification’s influence on our choices. For example, in a virtual hearing for the U.S. House of Representatives Committee on Financial Services, economist Vicki Bogan called for bans on user interface features in trading apps that are “designed to increase more trading volume without regard to consumer priorities or risks.” As noted above, IOSCO is considering similar measures.

Others say existing rules do too much — that they fail to recognize that even if gamification influences our choices, these choices are still technically ours to make. To avoid stifling innovation, apps need their own custom-built set of rules, like Ontario’s proposed gig worker regime.

Leveraging law’s flexibility

Both these lines of argument overlook the flexibility that’s built into law. We can interpret old rules in new ways to reflect the reality that gamification and other digital engagement tactics can have powerful influences over people’s behaviour — and that this influence can be wielded in perverse ways.

Instead of crafting new rules for trading app design, regulators can treat gamification tactics that nudge users into certain investments or trading patterns like tacit investment recommendations. To the extent these tactics work to guide clients into unsuitable investments and trading, regulators can jump into action with their existing rulebooks.

Rather than creating a new category of rights for gig workers, we can recognize that gig workers who are led to act like employees, whether through gamification or other tactics, should be treated as such. Luckily, Ontario’s proposals don’t preclude ongoing efforts to secure these rights through litigation.

Innovation and regulation

Calling for new rules before making full use of the ones we have isn’t just unnecessary. It’s potentially harmful. If we choose to interpret existing rules in rigid or technical ways, so that we have to create new rules for every new innovation, we’ll never catch up. As law falls further behind innovation, those who use technology to implement creative schemes for evading regulation will win out.

Gamification can do a lot of good, when deployed responsibly. It can make investing less intimidating. It can motivate users to learn new languages, new skills or healthier habits.

But apps shouldn’t be able to profit from shaping their users’ choices through gamification and then disclaim responsibility for these choices when regulators come knocking.

Law has tools for encouraging apps to exercise the influence they wield over their users’ choices in a responsible way. We just need to use them.![]()

Doug Sarro, SJD candidate and adjunct professor, Law, University of Toronto

This article is republished from The Conversation under a Creative Commons license. Read the original article.